Estimated reading time: 5 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

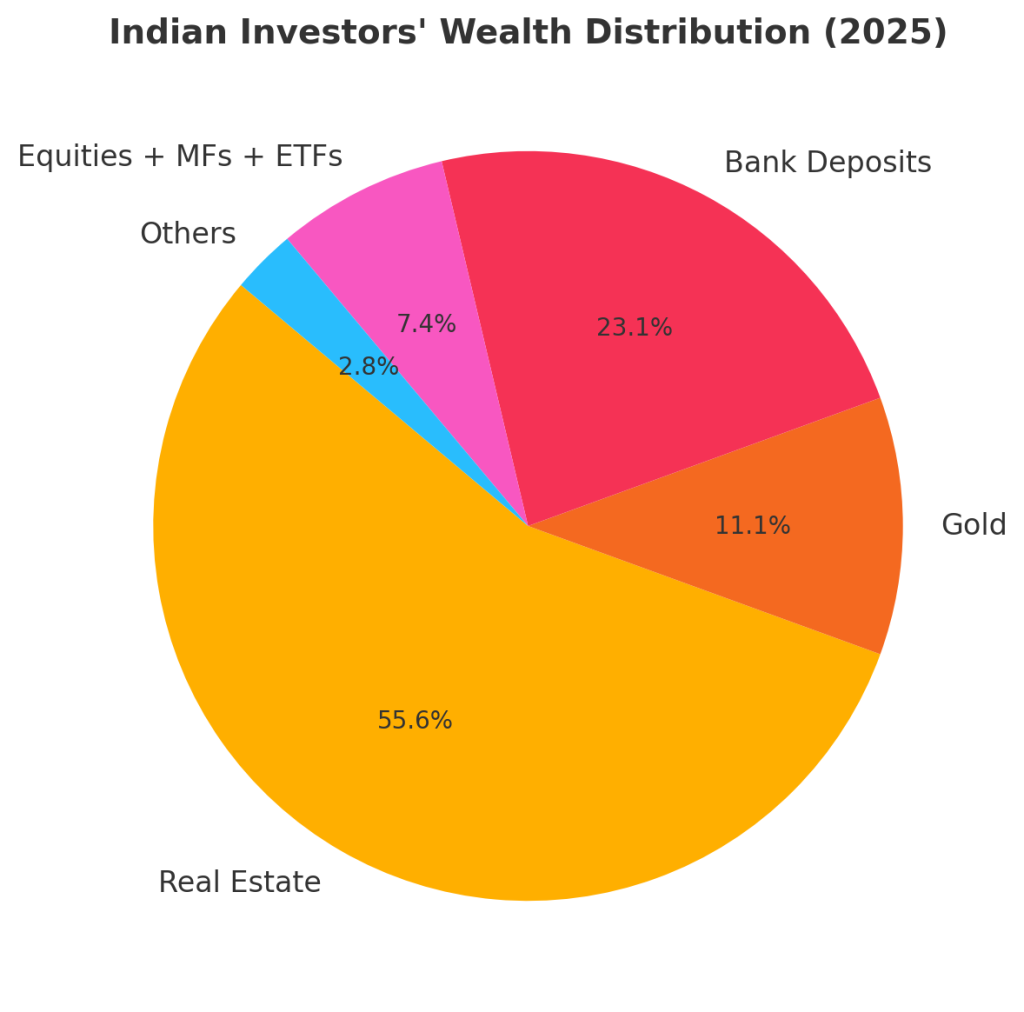

💰 Where is the Indian Investors’ Wealth:?

India is one of the fastest-growing economies in the world, and with rising incomes, savings, and financial awareness, investors are spreading their money across different asset classes. But the big question is: where does most of the Indian investors’ wealth actually sit?

📌 1. Traditional Favorites: Gold & Real Estate

- Gold has always been the “emotional investment” for Indians. From weddings to festivals, every family has gold in some form.

- India is the 2nd largest consumer of gold globally.

- Nearly 25,000 tonnes of household gold is estimated to be sitting idle in lockers!

- Real Estate is another big wealth absorber.

- For decades, buying land or property was seen as the safest way to grow wealth.

- Today, more than 60% of Indian household wealth is tied up in real estate.

📌 2. Bank Deposits – The Safety Net

- Fixed Deposits (FDs), Recurring Deposits (RDs), and Savings Accounts are still the most common choice for Indian investors.

- Around ₹180+ lakh crore is parked in bank deposits.

- Reason? Safety, guaranteed returns (though low), and easy liquidity.

- But here’s the catch → FD interest rates (4–7%) often fail to beat inflation.

📌 3. Stock Market – The Rising Star:

- Out of India’s total wealth, only 5–7% is directly invested in equities.

- However, the growth is explosive:

- Demat accounts crossed 150 million in 2025.

- SIP inflows in Mutual Funds hit ₹20,000+ crore per month.

- Investors are realizing that stocks & ETFs build long-term wealth better than gold or FDs.

📌 4. Mutual Funds – The Middle Path:

- Mutual Funds are now the bridge between traditional savers and stock market exposure.

- Assets under Management (AUM) crossed ₹60 lakh crore in 2025.

- SIP (Systematic Investment Plan) has become the new “savings habit” for young Indians.

- Equity MFs, Debt MFs, Hybrid MFs – people are diversifying based on goals.

📌 5. New-Age Assets:

- Digital Gold and Sovereign Gold Bonds (SGBs) are gaining popularity.

- REITs (Real Estate Investment Trusts) and InvITs are attracting urban investors.

- Crypto saw hype but remains volatile, with SEBI and RBI keeping strict watch.

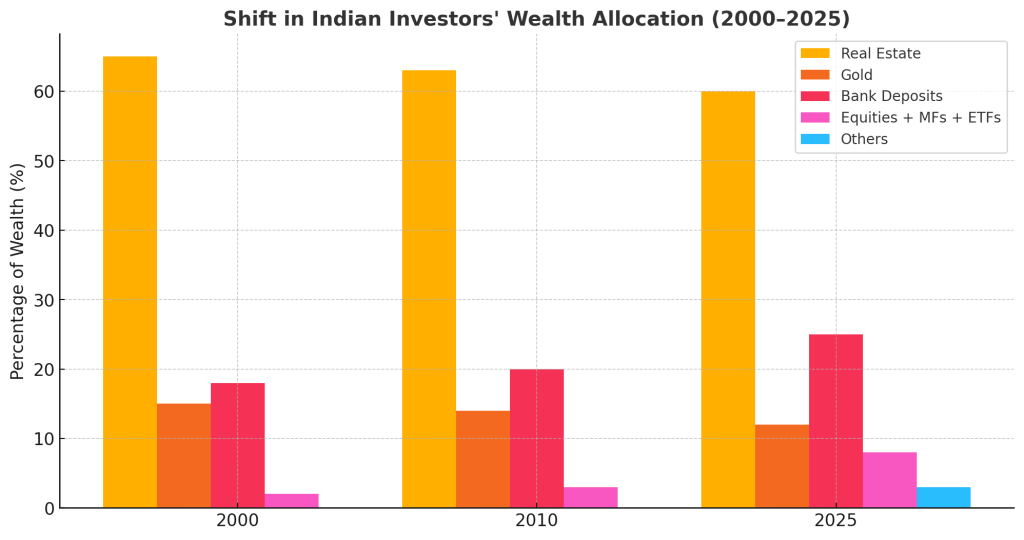

📊 The Big Picture – Where Indians Park Wealth (approximate 2025 data):

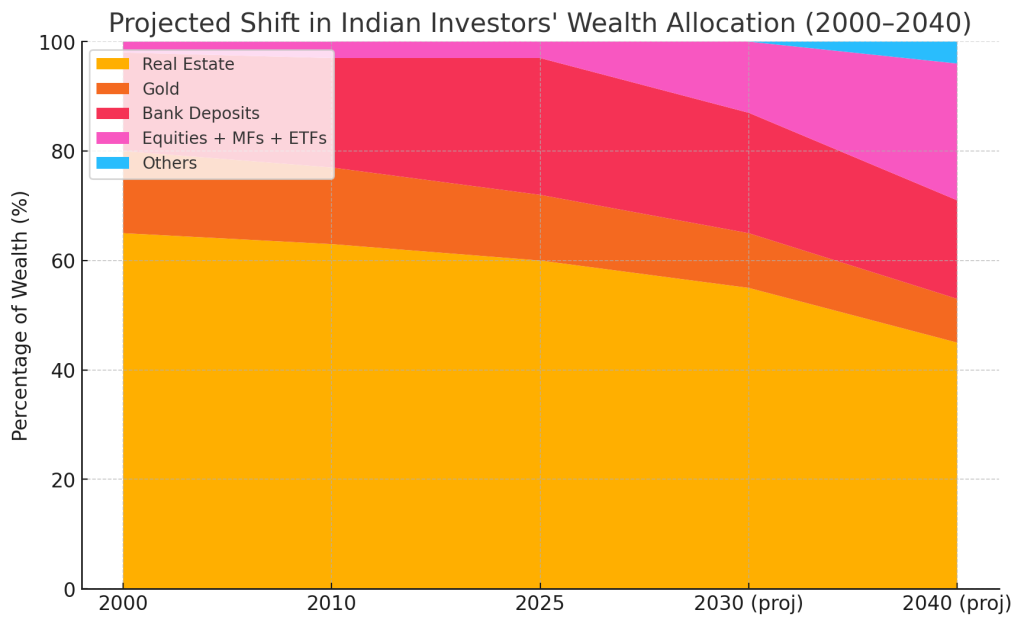

Key takeaway from the projection chart:

- Real estate share falls from ~60% (2025) to ~45% (2040).

- Equities + MFs + ETFs grow strongly from ~8% to ~25% by 2040 — showing younger investors shifting to markets.

- Bank deposits peak around 2025 then slowly decline.

- Gold slowly declines; “others” (REITs, digital assets) increase modestly.

Super question rey 👍 — even though stocks, ETFs, mutual funds are growing, Indians still love gold and real estate. There are some deep cultural + financial reasons for this. Here’s a structured explanation 👇

🏠 Why Indians Still Stick to Gold & Real Estate?

1. Cultural & Emotional Attachment:

- Gold is not just an investment, it’s tradition + status symbol.

- Weddings, festivals (Akshaya Tritiya, Diwali, Dussehra) → families buy gold every year.

- Real estate = izzat (prestige). Owning land/house gives social status in Indian families.

2. Physical & Tangible Security:

- People feel safer with something they can touch and see.

- Stocks are “invisible” → only numbers on a screen, which feels risky for older generations.

- A house or gold jewelry feels permanent and trustworthy.

3. Generational Habit:

- Parents & grandparents built wealth through land, property, and gold.

- They pass this mindset to the next generation: “Land and gold will never go waste.”

- Stock market is still seen as “speculation” in many towns and villages.

4. Lower Financial Awareness:

- Many people don’t understand equities, ETFs, SIPs, or compounding.

- But everyone understands: “If I buy land, its value will rise over years.”

- Lack of financial literacy → preference for simple, known assets.

5. Perceived Safety Against Inflation & Crisis:

- Gold acts as a hedge against inflation and global uncertainty.

- Real estate is seen as stable in long run — land is limited, demand always grows.

- People think: “Even if rupee falls, gold/land will still hold value.”

6. Easy Collateral for Loans:

- Banks easily give loans against gold or property.

- Stock market holdings don’t get the same trust.

- Families see gold/property as backup emergency funds.

7. Black Money & Unaccounted Wealth:

- Real estate and gold have historically been ways to park unaccounted money.

- Though rules are stricter now, the habit still continues.

8. Tax Treatment Favors Long-Term Holding:

🪙 Gold

- If you hold physical gold for more than 3 years, it is considered long-term capital asset.

- Long-term capital gains (LTCG) are taxed at 20% with indexation benefit (adjusts cost with inflation → lowers tax).

- Families often hold gold for decades, so tax burden becomes minimal.

🏠 Real Estate

- Property held for more than 2 years qualifies as long-term capital asset.

- LTCG on property also taxed at 20% with indexation.

- Additional benefit: Investors can use Section 54 exemption by reinvesting gains into another property → no tax at all.

👉 This makes real estate a preferred long-term generational asset.

📈 Equities (for comparison)

- Equity shares & equity mutual funds → LTCG (beyond 1 year) taxed at 12.5% (above ₹1 lakh gain per year).

- Short-term (less than 1 year) taxed at 20%.

So while equities have lower tax rates, real estate & gold enjoy indexation + exemptions, which many families see as a tax-efficient way to preserve wealth.

✅ Now the full picture looks stronger: cultural + emotional reasons + loan benefits + tax advantages all keep Indians heavily invested in gold and property.