Estimated reading time: 6 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

1. Swiggy Business Overview

Founded: 2014

Founders: Sriharsha Majety, Nandan Reddy, Rahul Jaimini

Headquarters: Bengaluru, India

Industry: Online food delivery & hyperlocal logistics

Core Business

Swiggy primarily operates in food delivery, connecting customers with restaurants through its app and website. But over the years, it has expanded into multiple verticals:

- Food Delivery (Core Business)

- Customers order food from partner restaurants via the Swiggy app.

- Swiggy delivers using its network of delivery partners (riders).

- Revenue comes from delivery fees, commissions from restaurants, and subscription services (Swiggy One).

- Grocery & Essentials (Swiggy Instamart)

- Instant delivery of groceries, daily essentials, and snacks.

- Focus on 10–30 minute deliveries in select cities.

- Hyperlocal Logistics & Other Services

- Swiggy Genie: Pick-up & drop-off service for packages, parcels, or personal errands.

- Cloud kitchens: Swiggy supplies kitchens for restaurants to reduce delivery time and expand reach.

- Swiggy Super / Subscription Services

- Monthly subscription giving free deliveries and discounts.

- Helps increase customer loyalty and recurring revenue.

Revenue Model

- Commission from restaurants – 15–30% per order.

- Delivery fees – Charged to customers (varies by distance/order size).

- Subscription fees – Swiggy One/Instamart subscription.

- Advertising – Restaurants pay for better visibility on the platform.

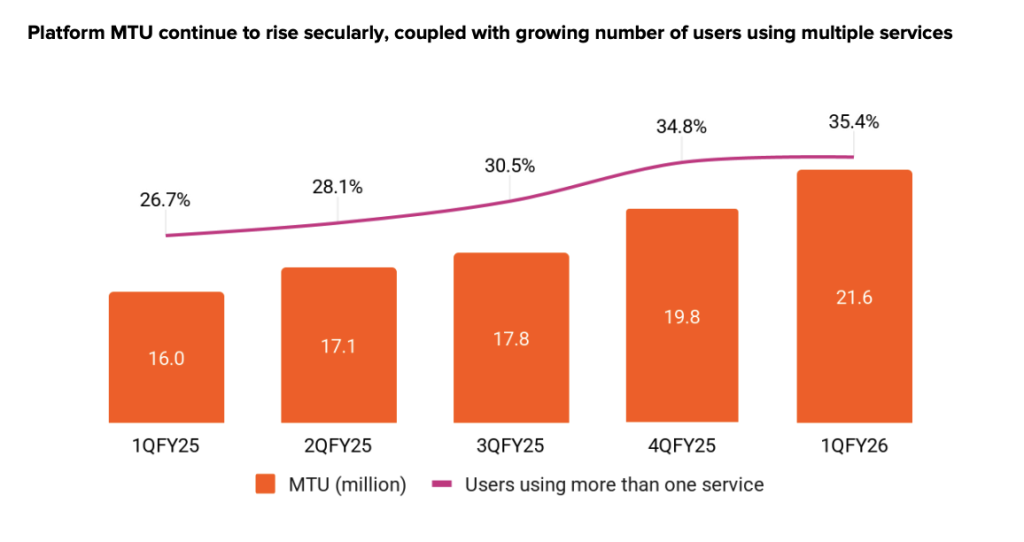

Highlights of the quarter

Swiggy Platform

○ Platform Average Monthly Transacting Users (MTU) grew 35.2% YoY to 21.6 Mn (+9.0% QoQ)

○ Consolidated Adjusted Revenue grew 52.7% YoY to INR 5,308 Cr (+12.5% QoQ)

○ B2C Adjusted EBITDA Margin (% of B2C GOV) declined by 204bps YoY to -4.7% (+12bps QoQ)

○ Consolidated Adjusted EBITDA loss increased by INR 81 Cr QoQ to INR 813 Cr

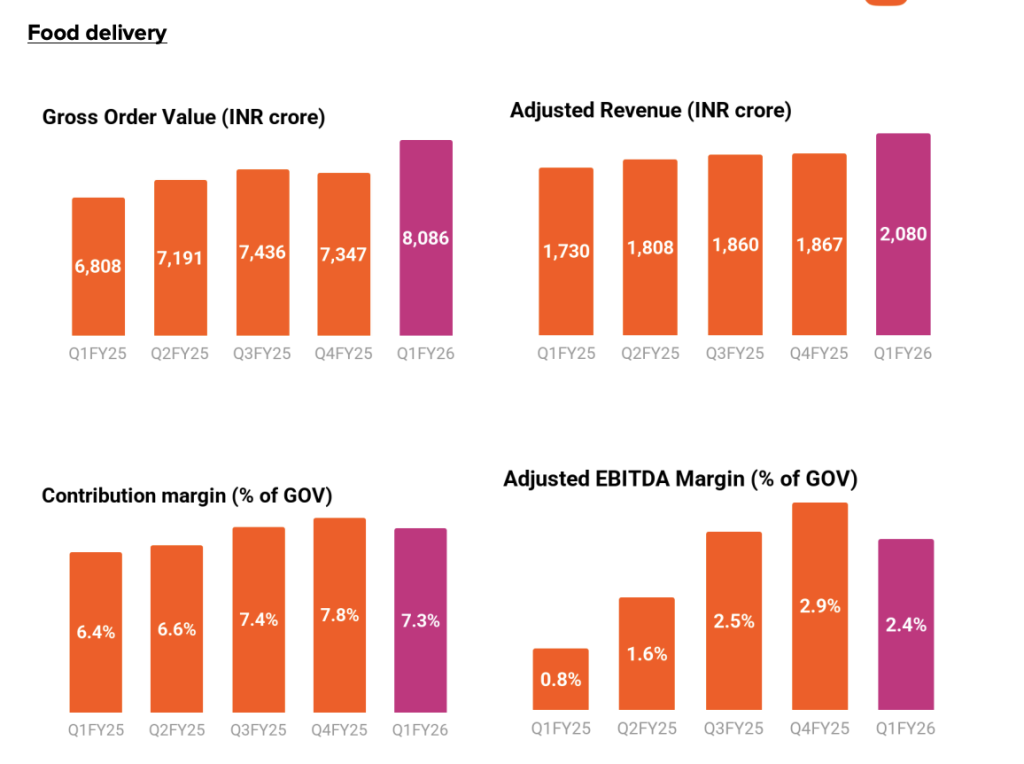

● Food delivery

○ GOV grew 18.8% YoY to INR 8,086 Cr

○ Added 1.2 Mn Monthly Transacting Users to reach 16.3 Mn, Maximum numbers of MTUs added

in a single quarter over the last 2 years

○ Adjusted EBITDA declined by 9.6% QoQ to INR 192 Cr, Adjusted EBITDA Margin at 2.4% of GOV

(+152bps YoY, -52 bps QoQ)

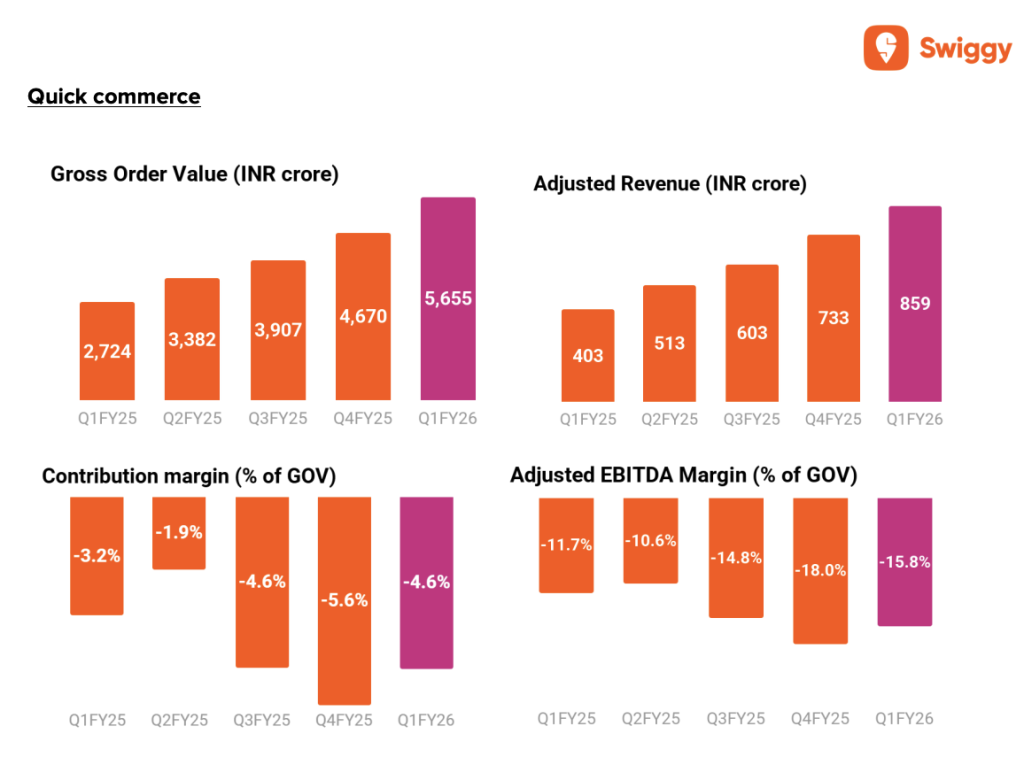

● Quick-commerce

○ GOV growth accelerated to 107.6% YoY (+21.1% QoQ) to INR 5,655 Cr, with 1.2 Mn MTUs added

(+12% QoQ)

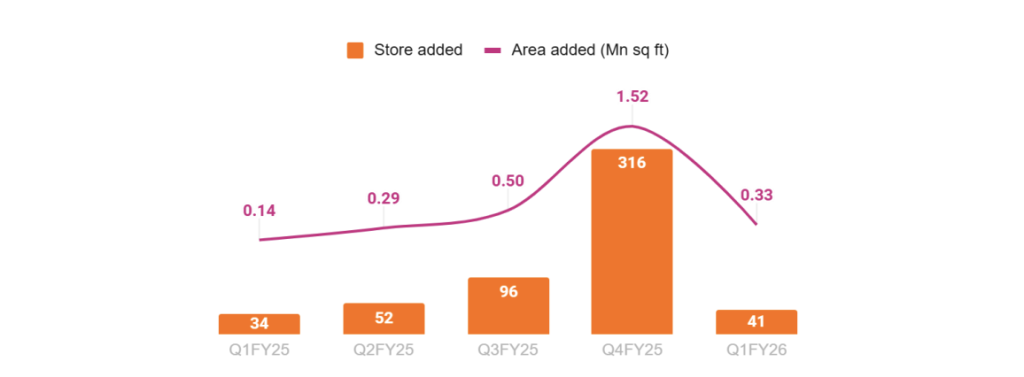

○ Added 41 darkstores, driving up active darkstore area to 4.3 Mn sq ft (+158.7% YoY, +8.2% QoQ),

growing average size of our darkstores further to over 4000 sq ft

○ Average order value grew 25.6% YoY to INR 612 ahead of our guidance, led by continued

expansion of non-grocery selection and larger-basket buying behaviour across user cohorts

○ Contribution margin improved by 97 bps to -4.6% in Q1FY26 in line with our guided trajectory

○ Adjusted EBITDA margin improved by 213bps (QoQ) to -15.8%.

Swiggy’s competitive landscape

1. Direct Competitors

a) Zomato

- Market Share: ~58% in food delivery in India; Swiggy has ~42%.

- Strengths:

- Strong brand recognition and first-mover advantage in many cities.

- International presence (Middle East, UAE).

- Diversified offerings: food delivery, Zomato Pro subscription, cloud kitchens, and grocery delivery (via acquisitions).

- Weaknesses vs Swiggy:

- Delivery network is slightly smaller in some Tier-2/3 cities.

- Customer experience varies depending on local delivery partners.

b) Zepto (Quick Commerce)

- Focus: Ultra-fast grocery delivery (10–20 minutes).

- Strengths:

- Extremely fast delivery using localized dark stores.

- Focused on millennial and Gen Z urban users.

- Challenges for Swiggy:

- Swiggy Instamart is slower (15–30 minutes) and slightly more expensive.

- High competition for small-ticket grocery orders.

c) Blinkit (by Zomato)

- Another major player in instant grocery delivery.

- Competes directly with Swiggy Instamart in metros and Tier-1 cities.

2. Indirect Competitors

- Regional/local food apps: FreshMenu, Box8, etc., mostly in metros.

- Supermarkets & online grocery: BigBasket, Amazon Fresh, Flipkart Supermart.

- Cloud kitchens & restaurant aggregators: Some restaurants operate their own delivery to bypass aggregators.

3. Key Competitive Factors

- Delivery Speed & Coverage

- Swiggy leverages a large delivery partner network, but Zepto and Blinkit offer faster grocery delivery.

- Tier-2 and Tier-3 city penetration is a growth area for Swiggy.

- Pricing & Discounts

- Heavy discounting is common across all platforms.

- Swiggy uses subscription plans (Swiggy One) to retain customers.

- Technology & Personalization

- Swiggy invests in AI for route optimization, personalized recommendations, and dynamic pricing.

- Zomato has a strong review and rating system, which helps in customer trust and retention.

- Brand Loyalty & Customer Retention

- Swiggy’s Swiggy One subscription builds recurring revenue and loyalty.

- Zomato uses loyalty programs like Zomato Pro and Gold.

- Profitability & Cost Management

- Food delivery is a low-margin business, and every player struggles to break even.

- Swiggy has higher operational costs due to wider delivery coverage and Instamart expansion.

4. SWOT Perspective vs Competitors

| Factor | Swiggy | Zomato | Zepto / Blinkit |

|---|---|---|---|

| Market Share (Food) | 42% | 58% | – |

| Market Share (Quick Commerce) | 26% | Blinkit 35% | Zepto 30% |

| Delivery Speed | Good | Good | Excellent for groceries |

| Pricing / Discounts | Moderate | Moderate | Aggressive in groceries |

| Tech / AI | Strong | Moderate | Moderate |

| Customer Loyalty | Swiggy One | Zomato Pro | Minimal |

Source: Screener.in

🧾 Key Financial Challenges

1. High Operating Costs

- Marketing Expenses: Elevated due to increased competition and customer acquisition efforts

- Employee Costs: Significant rise due to workforce expansion and operational scaling

2. Instamart’s Profitability Struggles

- Despite rapid growth, Instamart’s high operational costs and low margins have led to substantial losses, impacting overall profitability

3. GST Impact

- The recent imposition of an 18% GST on delivery fees has increased operational costs by approximately ₹180–200 crore annually. Companies like Swiggy are considering passing this burden onto delivery partners or customers, potentially affecting margins and order volumes

4. Market Volatility

- Swiggy’s stock has declined by 27% year-to-date, reflecting investor concerns over sustained losses despite revenue growth

🔍 Strategic Outlook

- Profitability Focus: Swiggy aims to achieve contribution breakeven in the quick commerce segment within the next 3–5 quarters

- Cost Management: Emphasis on balancing growth with sustainable cost management, especially in the quick commerce space

- Market Positioning: Continued investment in supply chain and infrastructure to support rapid delivery models and enhance customer experience

📊 Analyst Ratings & Price Targets

1. Motilal Oswal

- Rating: Buy

- Target Price: ₹560

- Upside Potential: ~32%

- Rationale: Positive macroeconomic factors, reduced competition, and improving profitability in the food delivery sector. The brokerage firm also noted signs of a turnaround in Swiggy’s quick commerce segment, Instamart.

2. TipRanks

- Average Price Target: ₹443.40

- High Estimate: ₹500

- Low Estimate: ₹382

- Upside Potential: ~3.44%

- Analyst Consensus: Strong Buy (based on 5 analysts)

3. TradingView

- Average Price Target: ₹462.67

- High Estimate: ₹740

- Low Estimate: ₹285

- Analyst Consensus: Buy (based on 25 analysts)

4. Trendlyne

- Average Price Target: ₹533.33

- Upside Potential: ~22.66% from the last price of ₹434.80

- Analyst Consensus: Outperform (based on 7 analysts)

5. Alpha Spread

- Average Price Target: ₹452.42

- High Estimate: ₹777

- Low Estimate: ₹287.85

- Upside Potential: ~4% from the average target

- Analyst Consensus: Buy (based on 24 analysts)

6. Yahoo Finance

- Average Price Target: ₹447.67

- High Estimate: ₹740

- Low Estimate: ₹285

- Analyst Consensus: Outperform (based on 24 analysts)

Technical analysis

More check in the video:

Disclaimer

This content is for informational purposes only and not financial advice. Investing in stocks involves risk—always do your own research or consult a financial advisor. Some links may be affiliate links, which may earn me a small commission at no extra cost to you.