Estimated reading time: 7 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

⚡ Power Grid Corporation of India Ltd — Business Model, Management View & Growth Outlook (2025-2030)

By Onetrader Guide

🧭 Introduction

Power transmission is the hidden backbone of India’s energy system: power generation gets the headlines, but it’s the grid which actually transports electricity from plant to consumer, ensures reliability and integrates renewables.

Power Grid Corporation of India Ltd (POWERGRID) is the country’s flagship transmission company — owning and operating much of the interstate transmission network and playing a central role in India’s energy transition.

In this article we’ll dig into how the business works, what management is saying, where the growth levers lie, what’s holding it back — and whether it deserves a place in a long-term portfolio.

Also Read: Fusion Micro Finance Ltd — Business Model, Management Insights & 2025–2030 Growth Outlook

🏢 Company Overview

- Name: Power Grid Corporation of India Ltd (POWERGRID)

- Core business: Planning, building, owning, operating high-voltage transmission lines (EHVAC/HVDC), substations, telecom infrastructure over its grid network.

- Market presence: Dominant share in India’s inter-state transmission system (ISTS) segment; also offers consultancy, telecom/optical ground wire services.

- Size & scale: Massive network, high reliability; a low-risk essential infrastructure business.

- Stock positioning: Large-cap, low growth relative to some peers, strong asset base, steady cash flows.

💡 Business Model — How POWERGRID Makes Money

1. Transmission Business (Core)

- POWERGRID builds transmission lines/substations under government/ISTS schemes.

- It then earns regulated transmission tariff (returns on capital cost + O&M) from its assets — giving stable, regulated income.

- Because many of its assets are long-tenor and essential, risk is relatively lower.

2. Project Execution & Asset Capitalisation

- For new lines/substations, POWERGRID undertakes EPC-style work or oversees contractors, invests capex, then capitalises assets and begins earning tariff.

- Speed of asset capitalisation drives revenue growth: more assets commissioned = more tariff income.

3. Non-core/Value-added Activities

- Telecom infrastructure (stringing fibre on transmission lines).

- Consultancy, design, system integration for other utilities (domestic & overseas) via its technical expertise.

- These segments add diversification and margin potential beyond the regulated transmission business.

4. Government & Renewable Transition Tailwinds

- India is increasing renewable capacity, which needs new transmission lines and removing bottlenecks.

- Mega-projects (HVDC links, green corridors) mean large future capex for transmission. POWERGRID is a key beneficiary.

🎙️ Management View & Strategy

- Management states they are “optimistic about long-term growth backed by India’s increasing electricity demand, grid modernisation and renewable integration.”

- They have indicated capex guidance for the next few years — e.g., a rising capex commitment in FY26/27/28 of ~₹28,000 cr / ₹35,000 cr / ₹45,000 cr respectively.

- Focus areas: faster asset capitalisation, reducing execution delays (Right-of-Way (RoW) issues, supply chain), efficiency in O&M, expanding non-core revenues.

Onetrader takeaway: Management is correct in pointing to the structural tailwinds; the key is execution — the delay in assets being commissioned is the main headwind the company flags repeatedly.

🧱 Competitive Moat — Why Power Grid Still Dominates India’s Transmission Sector

When you look at Power Grid, its moat isn’t flashy, but it’s deep and durable — built over decades through scale, regulation, and trust.

Here’s how the moat breaks down 👇

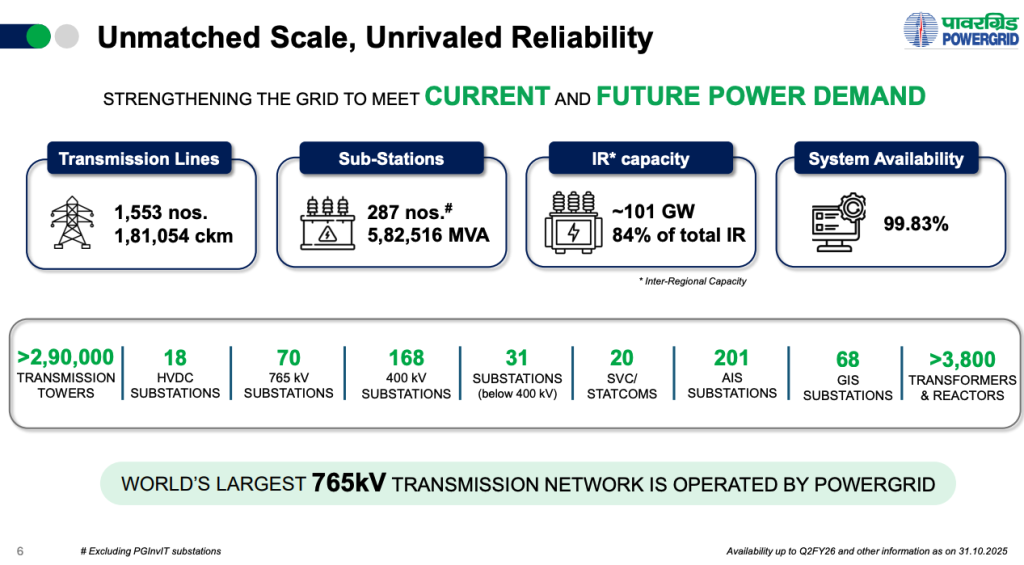

1️⃣ Natural Monopoly through Network Scale

- POWERGRID owns 85%+ of India’s interstate high-voltage transmission network (ISTS).

- Transmission is a network industry — once lines are laid and connected across the country, duplication is inefficient and uneconomic.

- Building a parallel network is practically impossible — both financially and environmentally.

✅ This makes POWERGRID a natural monopoly, protected by sheer physical scale and coverage.

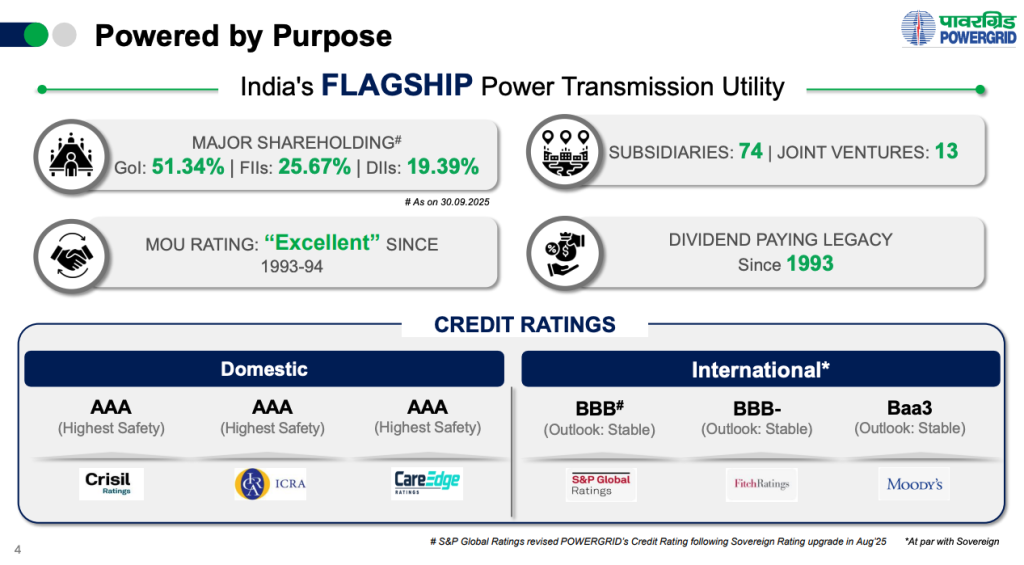

2️⃣ Regulatory Protection & Assured Returns

- Operates under regulated return-on-equity (RoE) framework approved by CERC (Central Electricity Regulatory Commission).

- Returns are guaranteed based on asset base (WACC + regulated equity) → stable earnings visibility.

- Even if demand fluctuates, POWERGRID’s revenue is assured via fixed tariff mechanism.

✅ This is a built-in economic moat — regulated monopoly with predictable returns.

3️⃣ Execution Experience & Technical Expertise

- Decades of project management expertise in HVDC, ultra-high-voltage AC systems, and renewable integration.

- Track record of delivering large projects (like ±800 kV HVDC Bipole lines, green corridors) within time & budget.

- Consultancy arm leverages this expertise internationally.

✅ Competence + reliability = huge barrier to entry.

4️⃣ Government & Policy Alignment

- Backed by Government of India (majority shareholder).

- In every new transmission plan or renewable corridor, POWERGRID is the first name chosen.

- Deep policy integration ensures continued project allocation.

✅ Strategic national importance = long-term policy support.

5️⃣ Financial Strength & Credit Advantage

- AAA credit rating → lowest borrowing cost in sector.

- Enables it to bid competitively and still maintain profitability.

- Competitors with higher borrowing costs can’t match its risk-adjusted returns.

✅ Financial moat from cost of capital advantage.

6️⃣ Technology & Digital Grid Readiness

- Smart grid management, SCADA, real-time monitoring, AI-driven maintenance analytics.

- Integration of renewable and grid-stabilizing technology (STATCOMs, synchronous condensers).

✅ Tech adoption ensures reliability and efficiency moat.

🏁 Onetrader Moat Verdict

| Type | Strength | Explanation |

|---|---|---|

| Network Scale | ⭐⭐⭐⭐⭐ | 85%+ grid share, impossible to replicate |

| Regulatory | ⭐⭐⭐⭐☆ | Fixed tariff ensures predictable cashflows |

| Execution Expertise | ⭐⭐⭐⭐☆ | 30+ years of proven large-scale projects |

| Financial Strength | ⭐⭐⭐⭐☆ | AAA credit, low-cost capital |

| Policy Alignment | ⭐⭐⭐⭐☆ | Government backing + strategic priority |

| Technology Integration | ⭐⭐⭐⭐☆ | Smart grid & digital advantage |

“POWERGRID’s moat is not speed — it’s structure.

It wins by being essential, regulated, and irreplaceable.”

🔮 Key Growth Drivers (2025-2030)

| Driver | Why it matters | Potential impact |

|---|---|---|

| Renewable integration / green corridor build-out | India’s renewable target demands transmission capacity to bring power from remote solar/wind parks to load centres | Big new lines + HVDC links → capex + tariff revenue |

| Asset capitalisation acceleration | More assets commissioned sooner = earlier tariff start | Revenue growth picks up |

| Non-transmission revenue growth | Telecom, consultancy, O&M services improve margin and reduce reliance purely on tariff | Diversified earnings mix |

| Efficiency improvements in O&M/cost | Lower cost → higher margins on existing asset base | Better return on equity |

| Government policy support / priority infra status | Transmission is a national priority; PGCIL has preferred market position | Market share advantage |

⚠️ Risks & Watch-points

- Execution delays / RoW / transformer supply bottlenecks: These reduce asset capitalisation and delay revenue. Management highlights these as key roadblocks.

- Regulated tariff risk & regulatory changes: While transmission is regulated, any adverse change in tariff framework or cost pass-through can hurt returns.

- Slow growth environment: If generation growth slows, or renewables stall, demand for new transmission may reduce.

- Debt & leverage risk: Large capex means large asset base and debt; while regulated, cost of finance and asset utilisation matter.

- Valuation complacency: Already a large scale business with modest growth; upside is limited unless growth execution improves.

🧾 Onetrader Verdict

POWERGRID is a strong, stable infrastructure franchise, ideal for investors seeking:

- Deep moat business (nationwide grid)

- Relatively low risk compared to other power/energy stocks

- Decent dividend yield + medium-term visibility

However, for investors seeking high growth, it may not offer explosive returns until execution speeds up significantly.

Recommendation:

- If your portfolio needs a “core infra / utility” hold for 5-10 years → POWERGRID fits well.

- Entry: Consider accumulating when valuation gives margin of safety or when asset capitalisation picks up visibly.

- Monitor the execution indicators (asset commissionings) & tariff frameworks.

Rating: ⭐⭐⭐⭐☆ (4/5)

Horizon: 5-10 years

Allocation style: Core “steady compounder” rather than high-growth bet.

❓ FAQ

Q1. What does Power Grid Corporation of India do?

A1. It owns and operates India’s interstate high-voltage transmission network, builds and runs transmission lines/substations, earns tariff on these assets and provides technical/consultancy/telecom services.

Q2. What are the biggest growth drivers for POWERGRID?

A2. Renewable integration requiring new transmission lines, speeding up asset commissioning, expanded non-transmission services, and government infrastructure push.

Q3. Is it safe to invest in POWERGRID?

A3. Reasonably safe — large scale, regulated business, strong brand and state backing. But growth is modest and execution risk remains.

Q4. What should an investor watch for?

A4. Quarterly asset capitalisations (new lines commissioned), tariff revisions/regulation, RoW & equipment supply delays, receivables from state utilities, margin trends.