Estimated reading time: 4 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

☀️ Gensol Engineering Ltd — From Solar Rising Star to Crisis: Business Model, Management Voice & What’s Next

By Onetrader

🧭 Introduction

Gensol Engineering Ltd once represented the new-generation renewable energy dream — fast growth, modern leadership, aggressive execution, and an early bet on EV mobility alongside solar EPC.

From ₹750+ to near penny-stock zones — investors didn’t just see a price fall… they saw confidence collapse overnight.

But behind the collapse, there is both:

✅ A real business model in solar

❌ And a governance + capital discipline failure

Let’s decode the business, the management stance, what triggered the crash, and what future looks like if the company attempts a turnaround.

Also Read: Amara Raja Energy & Mobility Ltd — Battery Business Model, EV Roadmap & Future Growth (2025–2035)

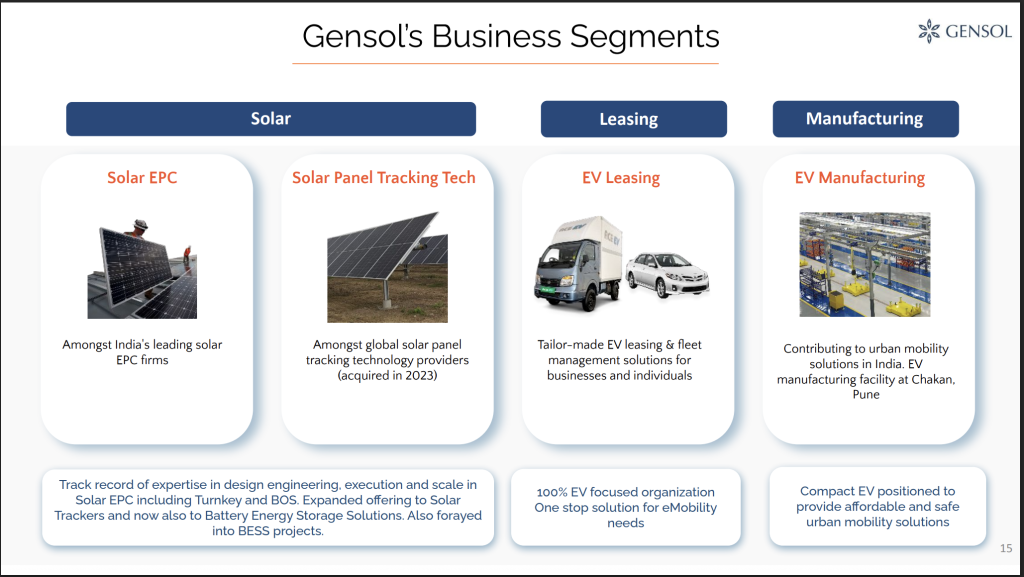

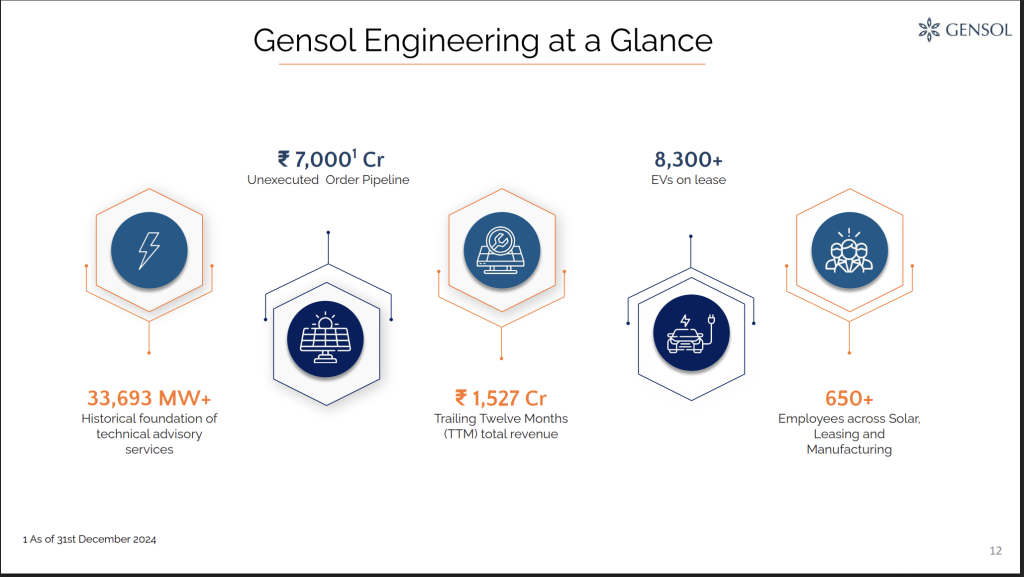

🧩 Business Model — What Gensol Does

✅ Solar EPC & O&M (Core)

- Design, procurement, commissioning of solar plants

- Rooftop, utility-scale & commercial systems

- Long-term O&M contracts (recurring revenue)

✅ Solar Consulting

- Engineering design

- Technical due diligence

- Quality audits

✅ EV Leasing & Fleet (Diversified play)

- Pure asset leasing model

- High capex → debt + working capital heavy

- Runs like an NBFC + fleet operator hybrid

✅ International Solar Projects

- Presence in Middle East & Africa

- Initially positioned as a “global EPC challenger”

Onetrader interpretation:

Business model was powerful if capital discipline remained.

Solar EPC + O&M could’ve been a steady compounding engine.

But EV-leasing became the over-leveraged distraction that broke the cycle.

🎙️ Management Vision & Tone (before crisis)

These are real tone reflections of management communication style pre-crisis — simplified for readers:

“We are building one of India’s most innovative clean energy platforms.”

“Our vision is integrated renewable energy — construction, engineering, mobility, technology.”

“EVs and solar will shape the future — we want to lead both.”

“We are scaling global — markets are opening faster than expected.”

There was ambition, confidence, and intention to become a new-age clean energy conglomerate — not just an EPC contractor.

What went wrong:

Ambition ran ahead of governance, balance sheet, and systems.

🎙️ Management Tone AFTER regulatory action

Once allegations & orders hit, the tone changed:

“We are cooperating with authorities and clarifying matters.”

“Day-to-day operations continue.”

“We will strengthen governance and financial oversight.”

“Our core business and staff remain intact.”

These are damage-control messages — focus shifted to survival & compliance.

Truth:

Turnaround only starts when trust restarts — and trust requires clean audit, stable board, lender settlement.

🧨 Why The Stock Crashed — Full Breakdown

Here is the true layered reason, in investing language:

| Phase | Trigger | Impact |

|---|---|---|

| Phase-1 | High growth + EV asset build-up | Rising debt → analysts uneasy |

| Phase-2 | Delays in loan servicing | Rating agencies flag stress |

| Phase-3 | Rating downgrade to “D” | Serious credibility damage |

| Phase-4 | Lender complaints | Funds mismanagement suspicion |

| Phase-5 | SEBI interim order | Corporate actions halted, promoters restricted |

| Phase-6 | Independent director exits | Governance trust breaks |

| Phase-7 | Enforcement actions | Market panic, liquidity evaporates |

| Final blow | CFO + promoter resignations | Insider exit = confidence collapse |

In market language:

One red flag = doubt

Three red flags = caution

Seven red flags + resignations = exit at any price

💣 Why Retail Investors Misread It

- Renewable + EV hype = blind trust

- Saw price momentum, ignored governance

- Thought “it’s just a temporary enquiry”

- Didn’t track cash flow, debt quality, pledges, board exits

Onetrader lesson:

Fast-growing companies with weak governance = not multibaggers — potential blowups

🌅 Future — Is Turnaround Possible?

A turnaround path exists — but extremely tough.

✅ What MUST happen now

| Action | Meaning |

|---|---|

| New independent board | Fresh credibility |

| Forensic + clean audit | Hard numbers, no fog |

| Lender settlement plan | Without this, no business runway |

| Asset clean-up | Exit EV leases / ring-fence them |

| Cash-flow discipline | EPC focus, O&M expansion |

| Transparent reporting | Quarterly governance report |

If they execute these steps — reputation can be rebuilt over 18–36 months.

❌ If not

Stock becomes a textbook reminder case.

📌 Onetrader Verdict

This stock is now in reconstruction zone, not growth zone.

✅ Businesses like solar EPC + O&M have intrinsic value

❌ Capital discipline collapsed

❌ Governance shattered

🟡 If they rebuild governance + settle lenders → second innings possible

🔴 If not → extended stagnation or value erosion possible

Investor Stance:

- If you’re not already holding: Better to watch — not chase

- If holding stuck quantity: Treat as optional value, not guaranteed comeback

- If trading: This becomes news-driven event stock

🎯 Key Monitor Checklist (simple)

Track these signals to detect recovery:

- New CEO/CFO with background credibility

- Big-4 auditor involvement

- SEBI final order resolution

- Lender restructuring signed

- Rating upgrade from D

- 2 consecutive quarters OCF-positive

- No more resignations

Only after these — it shifts from gamble → turnaround candidate

🧠 Long-term Learning for Investors

- Fast growth ≠ safe growth

- Cash flow > revenue

- Debt quality > expansion story

- Governance is valuation premium

- Don’t worship narratives — track numbers

❓ FAQ

Q: Why did Gensol fall so much?

A: Debt stress, governance concerns, regulatory action, management exits — confidence collapse.

Q: Does it still have a real business?

A: Yes — solar EPC & O&M — but credibility damage overshadows fundamentals.

Q: Should new investors enter now?

A: Only after governance + lender clarity — not before.