Estimated reading time: 7 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

🏥 Medi Assist Healthcare Services Ltd — Business Model, Management View & Growth Roadmap (2025–2030)

By Onetrader -Business Series

🔹 Snapshot

- Medi Assist is a technology-enabled health-benefits administrator (TPA/InsurTech) in India.

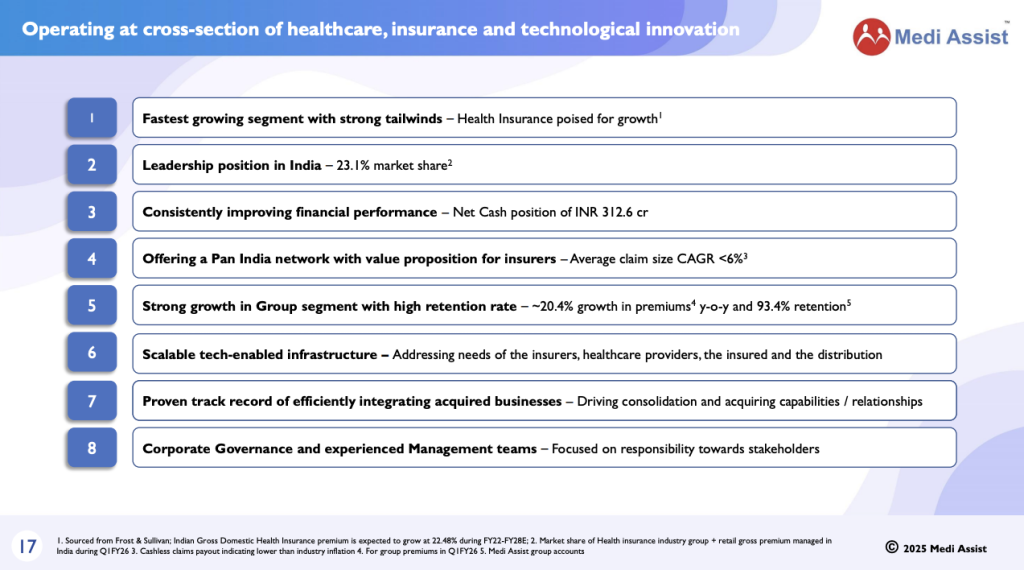

- It manages health insurance programmes, employee health-benefit schemes, retail health covers, and government health-schemes via its network of 18,000+ hospitals across 1,000+ cities & towns.

- Recently listed, with growth backed by higher premiums under management (PUM), digital technology investments, and insurance-ecosystem tailwinds.

- Credit rating: assigned CARE “AA-; Stable” rating for bank facilities recently — signalling financial strength.

- Key metrics: Q1 FY26 PUM ~ ₹7,076 crore (+18.5% YoY); Group segment PUM growth ~20.4% YoY.

Also Read: Gensol Engineering Crash & Recovery Roadmap — Business Model, Management Tone & Onetrader View

🔹 Business Model — How Medi Assist Makes Money

Medi Assist operates at the intersection of healthcare, insurance and technology. The business model is built on multiple pillars:

1. Third-Party Administration (TPA) of Health Insurance

The core business: Medi Assist acts as the administrator between insurers, hospitals/providers, policyholders and corporate/group accounts. For example: large employers outsource employee health benefits; Medi Assist handles claim processing, provider network management, cost control.

This engine generates recurring fees, and with scale the unit cost of administration falls.

2. Premium Under Management (PUM) Growth & Share-of-Wallet

Revenue is tied to premium under management — higher PUM means higher scale. Medi Assist’s reported PUM of ~₹7,076 crore in Q1 FY26 shows scale growth.

Also, market-share metrics: Group+Retail market share at ~23.1% as of June 30, 2025 (vs 21.3% a year ago).

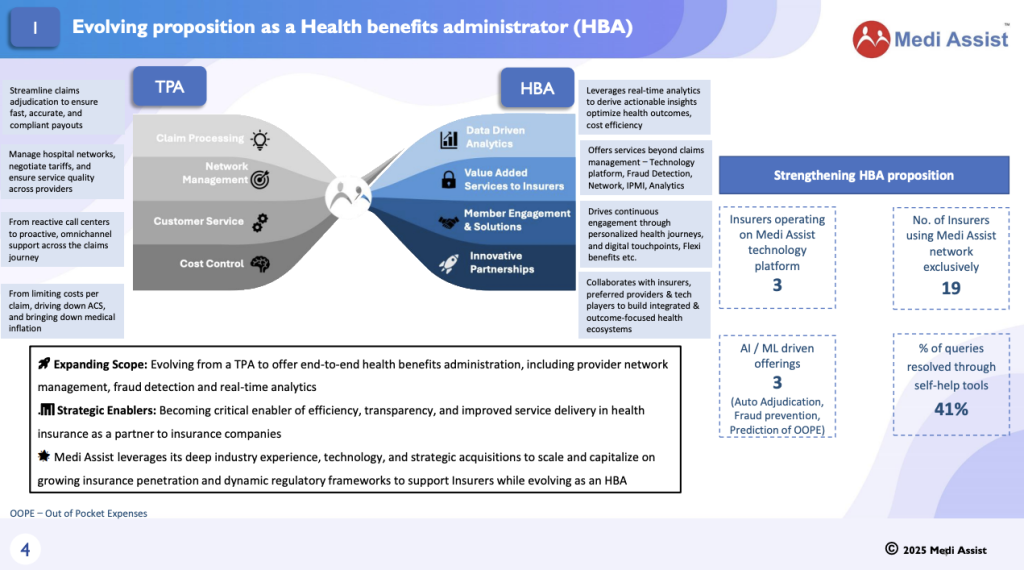

3. Technology, Analytics & Value-Added Services

Medi Assist emphasises tech-platforms: AI/ML for claims, fraud detection, digital onboarding, provider contracting, data-analytics. The “Products & Tech” page states the company invests in scalable infrastructure, secures operations and uses data to optimise outcomes.

This gives cost-efficiencies, differentiation, and some moats in a business where manual claims-processing can be a cost drag.

4. Network & Provider Partnerships

Operating with 18,000+ hospitals across 1,000+ cities ensures wide reach for employer and insurer clients. Such networks help maintain value for clients (employers/insurers) and hence retention.

Also the company has acquired/merged smaller TPAs (e.g., Medvantage, Raksha) which increases scale and consolidation benefits.

5. Diversification: Retail, Government Schemes, Employers

Beyond just corporate health covers, Medi Assist also services:

- Retail policyholders (via insurers)

- Public/State health-schemes

This diversification helps spread risk and opens multiple growth verticals.

Onetrader summary of model:

Medi Assist is effectively building a platform business: premium flows (via insurance) → network + admin services → technology + data → scale economics. In this niche, once scale is achieved, barriers to entry (network + tech + regulatory tie-ups) are moderate but growing. The key is capturing scale early and keeping cost-income ratio improving.

🎙️ Management View & Voice

From disclosures / investor presentations, here are the distilled views of management:

“We continue to strengthen our leadership position in the group segment and are building our retail, digital and government-scheme businesses for long-term growth.”

“We are investing ~5-7% of revenue in technology each year to deploy AI/ML, fraud detection, provider-contracting automation and claims efficiency.”

“Retaining large group accounts remains a key focus; our retention rate in the group segment for Q1 was ~93.4%.”

Management tone shows:

- Focus on retention + scale-up in group segment (stable foundation)

- Tech investment as strategic differentiator

- Aggressive growth in premium segments (PUM) and digital/retail channels

- Financial discipline: low debt, good liquidity, strong credit ratings

These signals indicate the company is not just chasing volume but building infrastructure for long-term profitability.

📊 Recent Performance & Signals

- Q1 FY26 results: Revenue growth +13.6% YoY; PAT growth ~18.7% YoY. PUM ~₹7,076 crore (+18.5% YoY).

- Financial strength: Debt-to-equity very low (near zero); credit rating CARE AA- assigned in March 2025.

- Network growth: 18,000+ hospitals across 1,069 cities (as of September 2023).

- A recent large strategic partnership: one of India’s largest retail health insurers decided to outsource sizeable claim processing to Medi Assist’s AI-driven platform — high-signal for technology advantage.

- Capital infusion: A foreign investor (MIT affiliate) invested ~₹198 crore through preferential allotment in Oct 2025 — shows investor confidence.

All these suggest Medi Assist is executing well: growing PUM, expanding network/tech, maintaining financial discipline.

🔮 Future Scope — 2025-2030 Roadmap

Medi Assist sits in a favourable structural tailwind: India’s health insurance penetration is low, employer-benefits market is rising, digital adoption is increasing, and cost-pressure on insurers/providers means more outsourcing to efficient TPAs.

Here’s how the next five years may shape:

A. Scale Growth & Market Share Gains

- Increase share of premium under management; from ~23% currently to perhaps 30%+ in group + retail segments by 2030.

- Grow retail PUM (currently slower) via direct partnerships and digital channels.

B. Tech/Analytics Become Moat

- AI/ML claims-processing and fraud detection reduce cost-income ratio → margin expansion.

- Deploy platform offerings (analytics subscriptions) for insurers/providers.

C. Provider Network Depth & Tier-2/3 Expansion

- Increase hospital network beyond 18,000 by reaching more Tier-2/3 towns, adding value-based partnerships (outcomes, cost optimisation).

- Deepening rural/employee-benefits markets.

D. Horizontal Expansion: Health-Ecosystem Services

- Wellness services, preventive health programmes, tele-health tie-ups.

- Vertical expansion into day-care/diagnostic administration via network partnerships.

E. Profitability & Return Enhancement

- With scale and tech leverage, return on capital employed (ROCE) currently ~18% can improve towards mid-20s by 2030.

- Retention and subscription-style revenues (analytics, outcomes-based service) can introduce margin stability.

Onetrader projection: Over next 5 years expect PUM growth ~15-20% p.a., revenue growth ~12-15% p.a., with margin expansion and strong financial metrics. The company merits “compounder with growth assurance” status in the healthcare-insurtech space.

⚠️ Risks & Watch-points

- Regulatory/IRDAI risk: As a TPA and insurer-ecosystem player, changes in regulations, fee-models, claim regulations could impact business.

- Provider contract risk: If hospital network contracts/reimbursements tighten, margin may suffer.

- Retail-segment slow growth: So far, retail PUM growth has been weak; retail segment is more competitive.

- Competition and commoditisation: Other TPAs, insurtech platforms may erode margins.

- Technology execution risk: Tech investments need to deliver; if cost remains high, profitability may lag.

🎯 Onetrader Verdict

Medi Assist is a very strong mid-to-long-term growth wealth-creation story:

- Leader in a growing, structural market (health insurance, employee benefits)

- Tech-enabled business with recurring revenue model

- Low debt, good financials, scale advantage

Strategy for investor:

- Consider as a core growth holding for 5–7 years.

- Monitor quarterly PUM growth, margin trend, tech cost ratio.

- Accumulate on dips where valuation aligns with growth.

Rating: ⭐⭐⭐⭐☆

Target horizon: 2025–2030

❓ FAQ (for blog)

Q1: What is Medi Assist’s core business?

A1: Medi Assist provides technology-enabled health benefit administration services, acting as a third-party administrator (TPA) for insurers, corporates (employee benefits) and government schemes, managing hospital networks, claims processing, prevention/wellness services.

Q2: Who leads Medi Assist and what is their vision?

A2: The management emphasises growing PUM (premium under management), investing in tech/analytics (~5-7% of revenue), and driving retention + scale in group & retail segments with strong network coverage.

Q3: Is Medi Assist a good long-term investment?

A3: Yes, for investors seeking exposure to health-insurance/insurtech growth in India. It has structural tailwinds, strong financials and scalable business model. Consider a 5–7 year horizon.

Q4: What are the key risks?

A4: Regulatory changes in health/insurance, cost pressure from provider payments, slow growth in retail segment, tech-execution risk, and competition.