Estimated reading time: 5 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

🔋 Amara Raja Energy & Mobility Ltd — The “Twin Engine” Battery Giant Powering India’s EV Future

By Onetrader Guide

🚀 Introduction

For decades, India’s battery industry has had two kings: Amara Raja and Exide.

When Indians talk car batteries, they don’t say battery… they say:

“Amaron unda…?”

That brand recall didn’t happen by chance — it happened through engineering, marketing, and timing excellence.

But today, Amara Raja is not just a battery company.

It is transforming into a new-energy powerhouse:

- EV & Lithium-ion cell manufacturing

- Gigafactory investments

- Energy storage solutions

- Powertrain systems

- Battery technology research

This is the “Lead-acid cash cow + Lithium-ion future bet” model — a rare dual flywheel business.

Let’s go deep. 🔍

Also Read : Colgate-Palmolive (India) Ltd — Business Model, Management Vision & Future Growth Outlook (2025–2030)

🧠 Company Snapshot

| Metric | Details |

|---|---|

| Company | Amara Raja Energy & Mobility Ltd (ARE&M) |

| Listed | NSE & BSE |

| Core Brands | Amaron, PowerZone |

| Legacy Strength | Automotive & Industrial Lead-Acid Batteries |

| Future Pillars | Lithium-ion, EV systems, Energy Storage |

| Capex Cycle | ₹9,500+ Cr over next few years for EV/Li-ion ecosystem |

| Export markets | 50+ countries |

💼 Business Model — Two Engines, One Vision

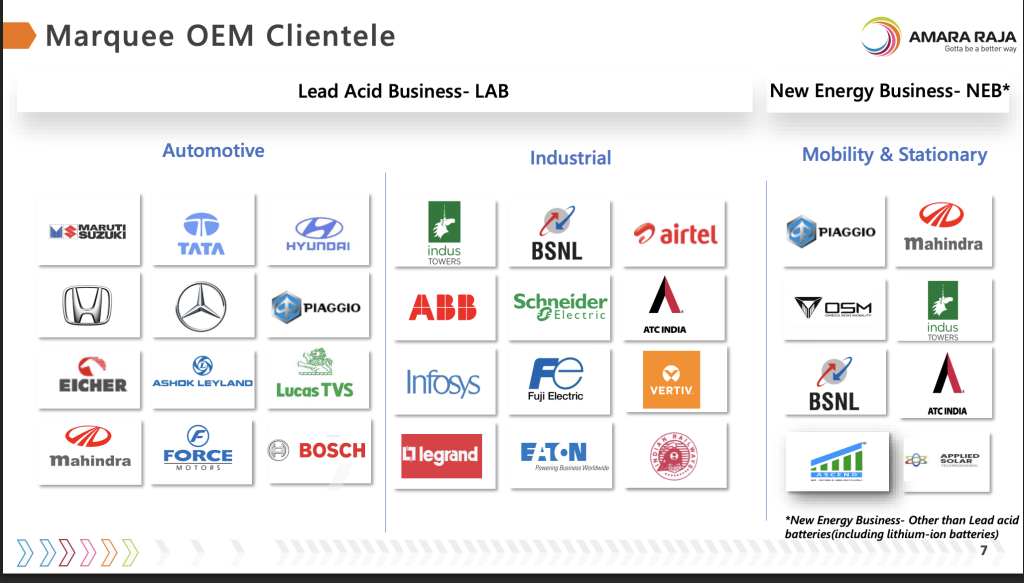

1️⃣ Core Business (Cash Machine) — Lead-Acid Batteries

Sectors served:

- Cars & 2-wheelers (OEM + replacement)

- UPS & Data Centers

- Telecom towers

- Railways & Defence

- Industrial backup systems

Why it’s strong:

- India’s ICE vehicle base is 15+ crore vehicles → constant replacement cycle

- Telecom & UPS demand rising (5G roll-out, digitization, data centers)

- Replacement market is high-margin recurring income

- Wide distributor network across India

Even with EV transition, lead-acid demand will exist for 15-20 more years, especially industrial & backup.

2️⃣ Future Business (Growth Engine) — Lithium & New-Energy Platform

Key focus areas:

| Segment | Vision |

|---|---|

| EV Cell Manufacturing | Gigafactory in Telangana (LFP technology pathway) |

| Battery Packs & BMS | For 2W/3W/LCV and stationary storage |

| Energy Storage Systems (ESS) | Solar + Wind integration for grid |

| Swappable battery solutions | Micro-mobility & logistics |

| Battery recycling | Closed-loop sustainability advantage |

Strategic partner: Gotion High-Tech (China) for Lithium-ion tech licensing — gives access to proven cell chemistry & gigafactory expertise.

This is India’s long-term battery war — and Amara Raja has placed its stake early.

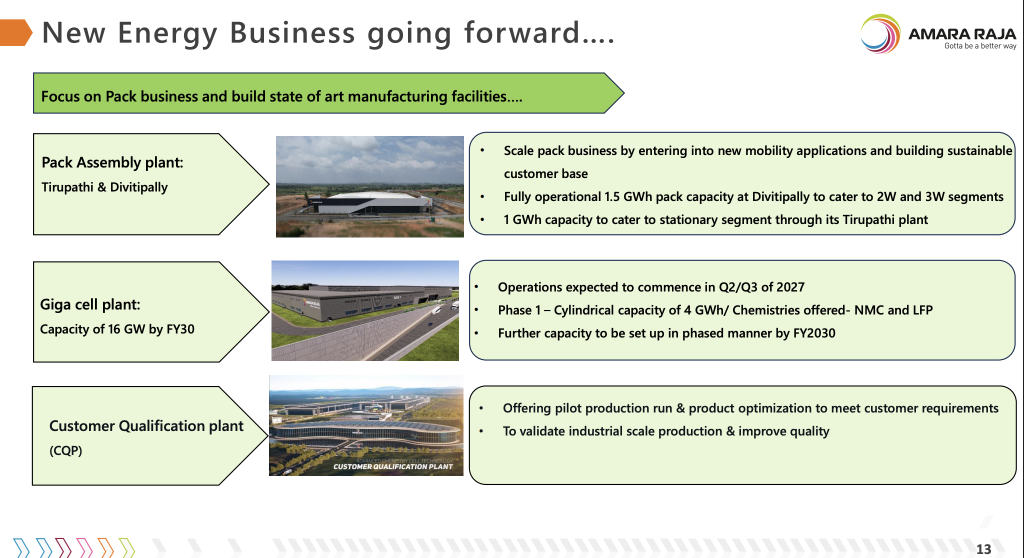

🏭 Gigafactory & Capex Vision

| Initiative | Detail |

|---|---|

| Gigafactory phase-1 | ~2 GWh capacity build-out |

| Final target | 16 GWh+ in phased manner |

| Investment plan | ₹9,500 Cr+ in Li-ion ecosystem (cell, packs, R&D, recycling) |

| Tech | LFP cells + future solid-state potential research |

This is a 10-year execution story — similar to Reliance New Energy roadmap.

🎙️ Management Thought Process & Tone

Vice Chairman Harshavardhana Gourineni:

“We are future-proofing Amara Raja — the next decade belongs to energy storage and electric mobility.”

MD Jayadev Galla:

“Lead-acid will remain important, but lithium is where we will build the next era of value.”

CEO on energy push:

“We are building India’s most trusted battery brand for both ICE and EV.”

Onetrader Interpretation:

They are balancing cash generation from old business while deploying capital into new-energy bet — a smart & disciplined play, not hype-driven.

Strengths

✅ Consistent profitability

✅ Strong cash flow from lead-acid business

✅ Low default risk, strong banking relations

✅ Healthy ROCE when normalized (legacy biz ~18–20% return profile)

Weakness

⚠️ Short-term ROCE may compress due to heavy capex & R&D

⚠️ Lithium business negative earnings for first few years (typical in energy transition phase)

🧭 Strategic Advantages (Moat Elements)

✅ Brand Strength & Distribution

- One of the most trusted battery brands in India

- Deep after-market presence & retail franchise network

✅ Dual Chemistry Manufacturing

- Lead-acid + Lithium capabilities

- Exide also has a Li-ion JV (with Leclanché) — India battery war is 2-player race

✅ Technology Partnerships

- Licensing deal with global battery leader Gotion High-Tech

- Investment in R&D for advanced chemistries

✅ Government Push Tailwind

- EV adoption

- Solar + storage push

- Data centers — UPS boom

- Railway electrification

🚧 Key Risks

| Risk | Impact |

|---|---|

| High Capex | Delays return on capital |

| Tech shift | Fast battery chemistry evolution (solid-state) |

| China supply reliance | Lithium cell & raw materials risk |

| Lead-acid decline pace | Faster EV adoption can compress legacy business faster than projected |

| Competition | Exide, Reliance New Energy, global players |

Mitigation: strong balance sheet, staged capex, local manufacturing push, recycling focus.

⏳ Amara Raja vs Exide — Onetrader View

| Factor | Amara Raja | Exide |

|---|---|---|

| Lead-Acid | Strong | Strong |

| Brand | Strong retail pull | Institutional + retail |

| Li-ion Strategy | Direct cell manufacturing vision | JV + pack strategy |

| Execution Speed | Aggressive | Slightly conservative |

| Brand Story | Challenger innovator | Giant incumbent |

Good thing?

This is not winner-takes-all. India’s battery TAM is huge.

Both can win — but execution speed = market share.

🔮 Future Roadmap (2025–2035)

1) Scale Gigafactory → 16+ GWh

Capacity = power. Scale lowers per-cell cost.

2) Pan-India EV battery pack solutions

Especially 2W/3W commercial fleets + charging ecosystem.

3) Recycling + Raw-Material Security

Battery recycling becomes a profit engine — like renewable fuel refineries.

4) Global expansion

Target Middle East, Africa, Southeast Asia — grid storage & telecom batteries.

5) Software + Battery management systems

AI-driven battery health monitoring → recurring SaaS-like revenue.

Onetrader Projection:

- Revenue CAGR 12–15% next 5 years

- EV battery contribution rises sharply 2027 onwards

- Inflection point: 2028–2030 when gigafactory scales

🎯 Onetrader Investment Verdict

This is not a “quick multibagger.”

This is a structural energy transition compounder.

Profile:

- ✅ Stable legacy cash flows

- ✅ High-capex, high-reward lithium pivot

- ✅ Execution-heavy but promising

Best suited for:

🔸 5–10 year horizon holders

🔸 Those bullish on India EV + storage theme

🔸 SIP accumulation on corrections

Rating: ⭐⭐⭐⭐☆

Strategy: Buy gradually on dips + hold long term

❓ FAQ (for blog)

Q1: What does Amara Raja do?

A: India’s leading battery company in automotive, industrial, and energy storage; now investing into EV lithium-ion gigafactory.

Q2: Will EV kill lead-acid batteries?

A: No — industrial & backup demand will sustain for many years, but EV lithium is the growth engine.

Q3: Is Amara Raja a good long-term stock?

A: Yes for long-term investors who understand capex cycles and EV storage market maturity.