Estimated reading time: 4 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

🟠 Hindustan Copper Ltd – Complete Business Analysis, Moat, Management Strategy & 2025–2035 Outlook

By Onetrader Guide

🧭 Introduction

Hindustan Copper Ltd is India’s only vertically integrated copper ore mining company and a strategic PSU under the Ministry of Mines.

Copper is no longer just an industrial metal.

It is the backbone of:

- Electrification

- Renewable energy

- Electric vehicles

- Power transmission

- Data centres

- Defence & railways

This makes Hindustan Copper a strategic national asset, not just a commodity company.

Also Read: HBL Engineering Ltd – Business Model, Railway Safety Moat & Long-Term Outlook

🏢 Company Overview

| Parameter | Details |

|---|---|

| Founded | 1967 |

| Ownership | Government of India (~66%) |

| Sector | Mining & Metallurgy |

| Core Product | Copper ore, concentrate, cathodes |

| Operations | Rajasthan, Jharkhand, Madhya Pradesh |

| Nature | Mining + Smelting (integrated) |

HCL is the only PSU in India with copper mining rights and integrated processing capability.

⚙️ Business Model – How HCL Makes Money

HCL operates across the entire copper value chain:

- Exploration & Mining

Copper ore extracted from captive mines - Beneficiation

Ore → copper concentrate - Smelting & Refining

Concentrate → copper cathodes - Sale to End Users

Power, cables, EVs, transformers, defence, railways

This integration reduces raw-material risk compared to pure smelters.

🪨 Mining Operations (Core Asset)

Major Mining Locations:

- Khetri Copper Complex (Rajasthan)

- Malanjkhand Copper Project (Madhya Pradesh)

- Indian Copper Complex (Jharkhand)

These mines give HCL strategic domestic supply, reducing import dependence.

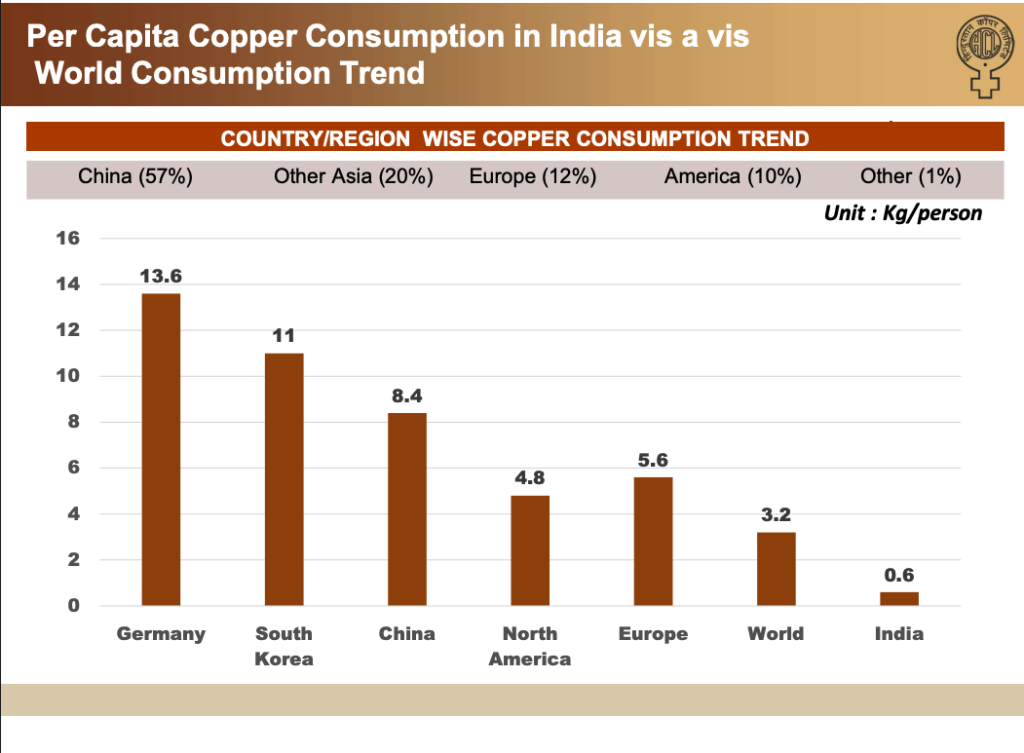

🔌 End-Use Demand Drivers (Why Copper Is Strategic)

Copper demand is exploding due to:

- EVs (4× copper vs ICE vehicles)

- Renewable energy (solar, wind, storage)

- Power transmission & grid expansion

- Data centres & digital infrastructure

- Defence & railways

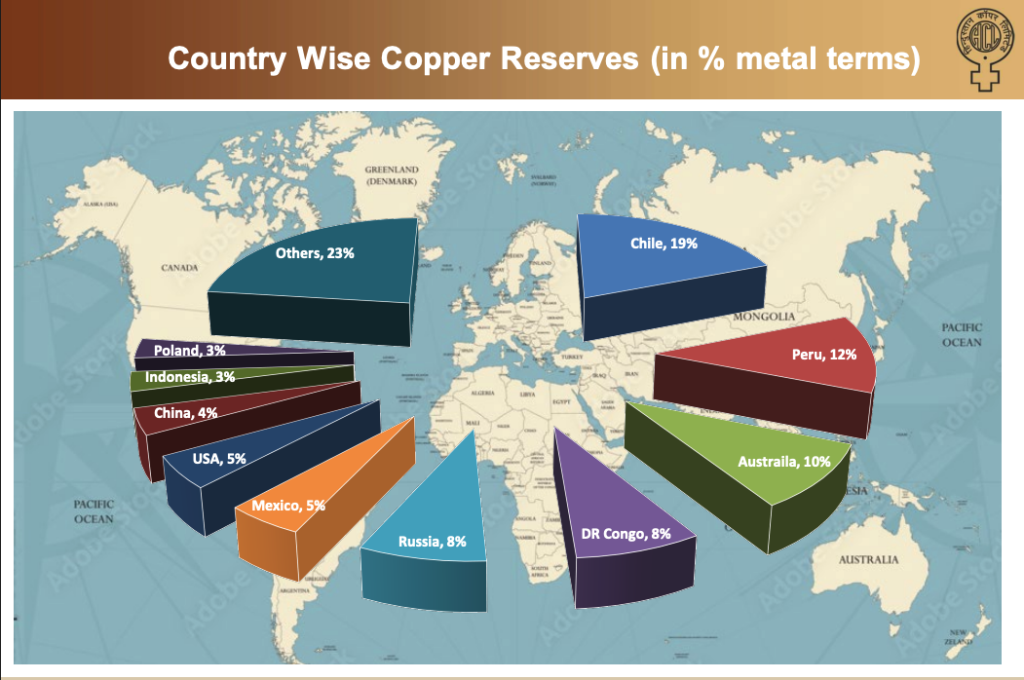

India currently imports ~90% of copper requirement → HCL’s role becomes critical.

🧱 Moat – Why Hindustan Copper Is Unique

⭐ 1️⃣ Monopoly in Copper Mining (India)

HCL is the only domestic copper miner.

No private player has mining rights at scale.

⭐ 2️⃣ Strategic PSU Status

Government support for:

- Mining leases

- Expansion approvals

- Strategic minerals

Copper is treated as a critical mineral.

⭐ 3️⃣ Vertical Integration

Mining → refining → cathodes

This lowers cost volatility compared to import-dependent smelters.

⭐ 4️⃣ High Entry Barriers

Copper mining requires:

- Geological expertise

- Environmental approvals

- Decades of capex

- Long gestation

New entrants are almost impossible.

⭐ 5️⃣ Long-Life Assets

Copper mines can operate for 30–50 years.

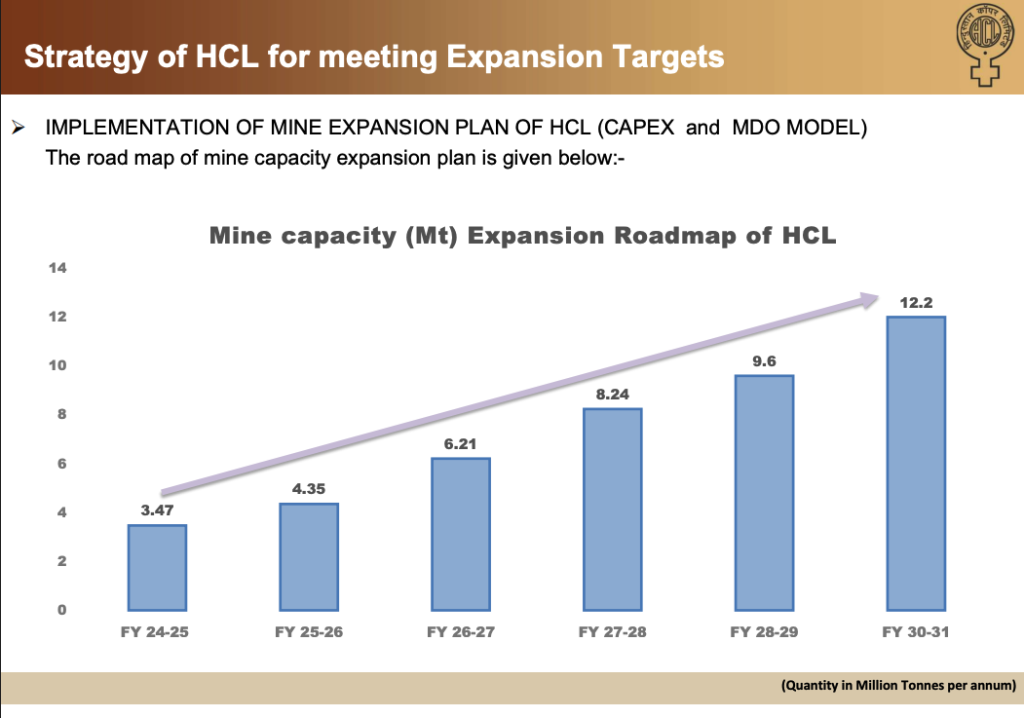

🧑💼 Management Commentary & Strategic Thinking (IMPORTANT)

You were right earlier — so this section is mandatory now 👇

🎯 Management Vision (Onetrader Interpretation)

HCL management has clearly stated its goal:

To triple ore production over the next decade.

This is not short-term optimism — it is backed by:

- Mine expansion plans

- New shafts

- Underground mining tech

- Brownfield expansions

🔍 What Management Is Focusing On

1️⃣ Volume Expansion Over Price Speculation

Management is not betting on copper prices.

They are betting on:

- Higher domestic production

- Better mine utilization

- Lower unit costs

2️⃣ Reducing Import Dependence

India’s copper deficit is a policy concern.

HCL is positioned as:

- Strategic supplier

- Import substitution enabler

This aligns with Make in India.

3️⃣ Modernising Legacy Assets

HCL is upgrading:

- Old shafts

- Mining equipment

- Beneficiation technology

Goal: improve recovery & margins.

4️⃣ Disciplined Capex

Capex is:

- Phased

- Project-linked

- Government approved

Avoids reckless expansion.

🧠 Onetrader Take on Management

✔ PSU-style conservative

✔ Long-term planners

✔ No hype-driven commentary

✔ Focus on volumes & execution

This is execution-first management, not market-facing.

📊 Financial Characteristics (Conceptual)

HCL shows:

- Revenue sensitivity to copper prices

- Operating leverage when prices rise

- PSU-level margins (moderate)

- Capex-heavy but long-life assets

- Improving ROCE with scale

This is cyclical + strategic, not FMCG-like.

🚀 Growth Drivers (2025–2035)

🚀 1️⃣ Copper Demand Supercycle

EVs, renewables, grid expansion = structural demand.

🚀 2️⃣ Capacity Expansion

Planned ore production increase → revenue growth.

🚀 3️⃣ Import Substitution Policy

Government backing for domestic minerals.

🚀 4️⃣ Defence & Railways

Strategic copper supply to national projects.

🚀 5️⃣ Global China+1 Theme

Global supply chain diversification boosts copper value.

⚠️ Risks You Must Understand

⚠ Commodity price volatility

⚠ PSU execution delays

⚠ Environmental & land approvals

⚠ Capex overruns

⚠ Operational risks (mining accidents)

These are structural mining risks, not company-specific red flags.

🔍 Hindustan Copper vs Other Copper Players

| Company | Nature |

|---|---|

| Hindustan Copper | Mining + refining (domestic monopoly) |

| Vedanta | Smelting, no mining |

| Hindalco | Aluminium-focused, copper refining |

| Global miners | Large-scale but not Indian |

HCL’s mining monopoly is the key differentiator.

🎯 Onetrader Final Verdict

Hindustan Copper is not a trader’s stock.

It is a strategic commodity + national asset play.

Best suited for:

✔ Long-term investors

✔ Those bullish on electrification & EVs

✔ Investors understanding commodity cycles

✔ Portfolio exposure to critical minerals

Onetrader Rating: ⭐⭐⭐⭐☆ (4/5)

Category: Strategic Commodity PSU

Theme: Copper Supercycle + Energy Transition