Estimated reading time: 5 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

💰 Fusion Micro Finance Ltd — Empowering Rural India, Building Financial Inclusion

By Onetrader

🧭 Introduction

When you think of India’s financial system, big banks dominate the news — but the real financial inclusion happens in the villages, where people borrow ₹20,000 to ₹50,000 to start a shop, buy livestock, or grow crops.

And that’s where Fusion Micro Finance Ltd (Fusion) has made its mark.

Fusion isn’t a flashy fintech startup; it’s a grassroots lender, operating deep inside rural and semi-urban India, empowering women entrepreneurs and micro enterprises through small but meaningful loans.

Backed by strong institutional investors and professional management, Fusion is one of India’s leading NBFC-MFIs (Non-Banking Finance Company – Micro Finance Institution).

🏢 Company Overview

| Parameter | Details |

|---|---|

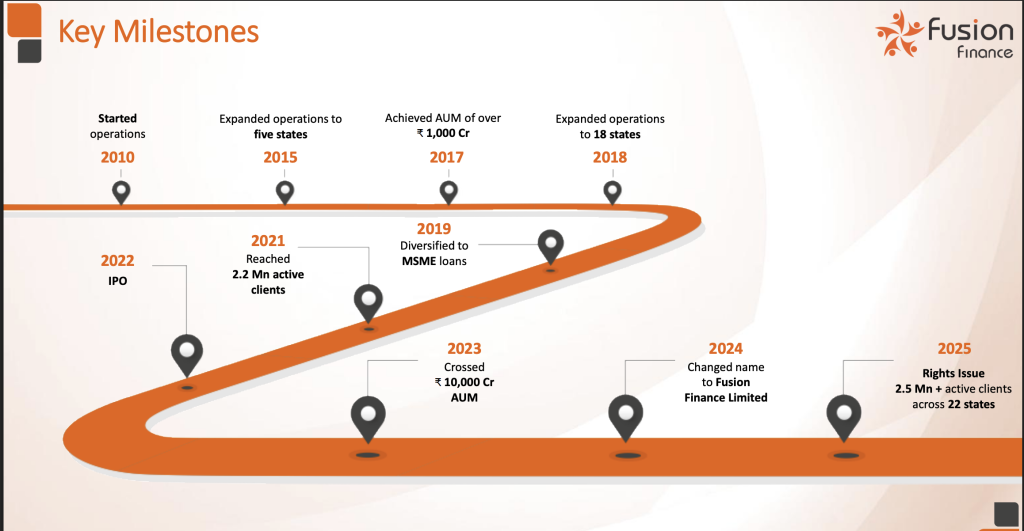

| Founded | 2010 |

| Headquarters | Gurugram, Haryana |

| Listing | November 2022 |

| Sector | Microfinance / NBFC |

| Promoter | Devesh Sachdev (Founder & CEO) |

| Clients | Low-income women borrowers (mostly in rural/semi-urban India) |

| Loan size | ₹30,000 – ₹80,000 average |

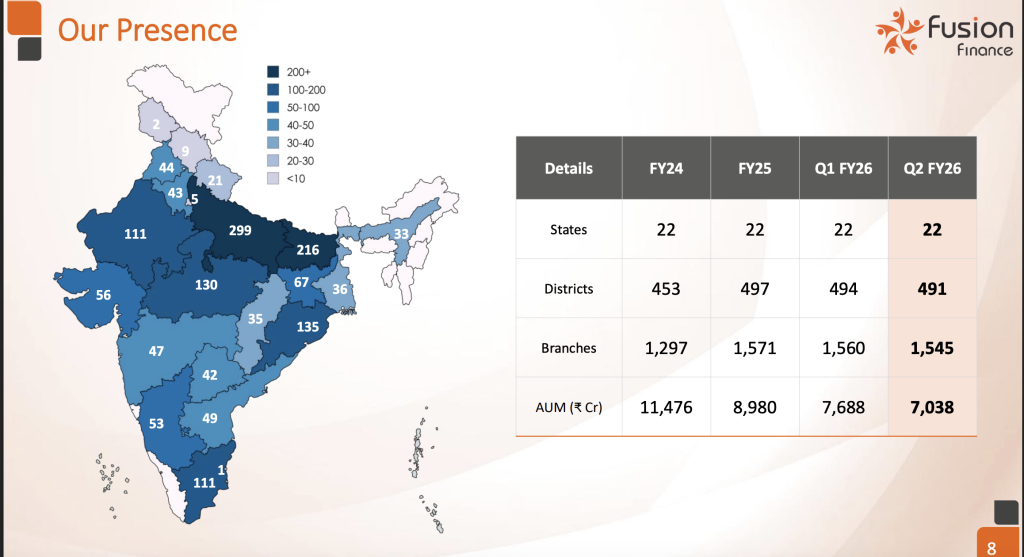

| Presence | 20+ states, 1,000+ branches, 40 lakh+ customers |

💡 Business Model — How Fusion Makes Money

Fusion provides small-ticket unsecured loans to women in low-income households through the Joint Liability Group (JLG) model.

Key Revenue Streams

1️⃣ Microloans to Women Borrowers

- Loans for livelihood, dairy, shops, tailoring, and farming

- Group lending ensures social repayment pressure

- Average tenure: 1.5–2 years

- Average ticket size: ₹30,000–₹70,000

2️⃣ Cross-Selling Insurance Products

- Life & credit insurance attached to loan products

- Earns commission income

3️⃣ Fee Income from Partnerships

- Ties with banks/NBFCs for co-lending

- Earns service/processing fee

Business logic: High-yield, short-tenor, high-rotation loan book.

Margins are strong but risk must be managed through borrower selection & local monitoring.

Also Read: Bajaj Housing Finance Ltd — Business Model, Management Insights & 2025-2030 Growth Outlook

🔐 How Fusion Controls Risk

- Group lending model: Borrowers support each other, ensuring repayments.

- Local field officers: Deep relationships with customers.

- Data-driven underwriting: Geo-based credit scoring.

- Insurance coverage: Life and loan insurance on borrowers.

- Diversified book: Pan-India presence reduces regional shocks.

🎙️ Management Vision & Culture

Devesh Sachdev, Founder & CEO, is known for his clear focus on responsible lending.

He often says:

“Microfinance is not charity — it’s dignity finance. Our job is to help people grow without creating debt traps.”

“We invest heavily in field training, risk management, and customer education.”

The management tone is mature, socially aware, and risk-focused — a blend that has helped Fusion survive multiple stress cycles (demonetisation, COVID, floods, etc.).

📈 Financial Performance Snapshot (FY24 – FY25 Trends)

| Metric | FY24 | Growth / Comment |

|---|---|---|

| Loan Book | ₹10,700 Cr+ | +27% YoY |

| Active Clients | 40 Lakh+ | Rising rapidly |

| GNPA | ~2.3% | Stable, well-managed |

| ROE | ~15% | Improving steadily |

| Capital Adequacy | 22%+ | Strong |

| Disbursements | ₹4,500 Cr+ | Growing quarterly |

Fusion is in growth mode, but with controlled risk and improving profitability.

🔮 Future Growth Drivers (2025–2030)

| Growth Engine | Description |

|---|---|

| Expanding Rural Penetration | Targeting untapped semi-urban & Tier-3 towns |

| Technology in Credit | AI-based borrower evaluation + digital collection tools |

| Cross-Sell | Insurance + financial literacy programs |

| Diversified Funding | Tapping banks, DFIs, securitization lines |

| Women Empowerment Programs | Government & NGO tie-ups boosting borrower base |

Fusion’s strength lies in its reach + trust — a powerful combo in rural credit markets.

💬 Promoter & Institutional Holding

- Promoter: Devesh Sachdev continues to hold ~63% along with investor funds.

- Institutional Shareholders: Global investors like IFC, Warburg Pincus, Honey Rose Investment, and others have backed Fusion.

- Governance Quality: Board includes independent directors & global investors’ representatives.

✅ High promoter commitment + strong institutional discipline = balanced ownership structure.

🔻 Possible reasons for the recent fall

- Credit / NPA concerns — Micro-finance companies are exposed to rural income shocks (weather, crops) and unsecured loans. If market fears increasing NPAs, valuation takes a hit.

- Funding cost inflation — If interest rates rise or access to low-cost funding becomes tight, margin gets squeezed. Investors may pre-empt this.

- Regulatory changes — RBI / Microfinance-regulator policy changes (caps on rates, recovery norms) could weigh future earnings.

- Rural economy slowdown — If consumption/loan demand in semi-urban/rural India slows, growth in book could decelerate and market may punish.

- Valuation pressure / profit booking — After strong run-up, some investors may have booked profits, causing a pull-back.

- Company-specific update — Possibly a weak quarter, higher costs (tech/collections), or investor concern about execution could trigger fall.

⚠️ Key Risks

| Risk | Impact | Mitigation |

|---|---|---|

| High credit risk (unsecured) | NPA volatility | Strong group-lending discipline |

| Weather & regional shocks | Rural borrowers’ vulnerability | Geographic diversification |

| Regulatory changes | Could limit lending rates | Track RBI microfinance guidelines |

| Funding cost increase | Could pressure margins | AAA-rated borrowings & securitization lines |

Fusion’s ability to control NPAs during stress years will define long-term compounding.

🎯 Onetrader Verdict

Fusion Micro Finance = Rural growth + Responsible governance + Long runway.

✅ Large untapped borrower base

✅ Strong management & promoter holding

✅ Healthy growth + improving profitability

✅ Institutional backing ensures discipline

❌ Cyclical risk if rural income drops

❌ Needs capital efficiency focus as book grows

Onetrader View:

⭐ Solid 5–7 year compounder in the financial inclusion theme.

⭐ Not risk-free, but well-managed in a tough segment.

⭐ Suitable for investors comfortable with NBFCs.

❓ FAQ

Q1. What does Fusion Micro Finance do?

A: It provides small-ticket loans to women entrepreneurs in rural and semi-urban India through the joint liability group (JLG) model.

Q2. Who leads the company?

A: Devesh Sachdev, Founder & CEO, known for his strong microfinance discipline and customer-first approach.

Q3. Is Fusion Micro Finance profitable?

A: Yes — consistent profits, strong growth, and improving return ratios.

Q4. Is it safe for long-term investment?

A: Moderate risk, strong governance. Good for patient investors in financial inclusion space.