Estimated reading time: 4 minutes

Thank you for reading this post, Please bookmark onetrader.in website for regular updates!

🏡 Bajaj Housing Finance Ltd — Business Model, Management Vision & Future Growth Outlook (2025–2030)

By Onetrader Guide

🧭 Introduction

When we talk about Indian financial institutions, Bajaj Group stands in a league of its own — conservative credit culture, high governance standards, and a proven track record in lending cycles.

Inside this group, one company is quietly building into a lending powerhouse:

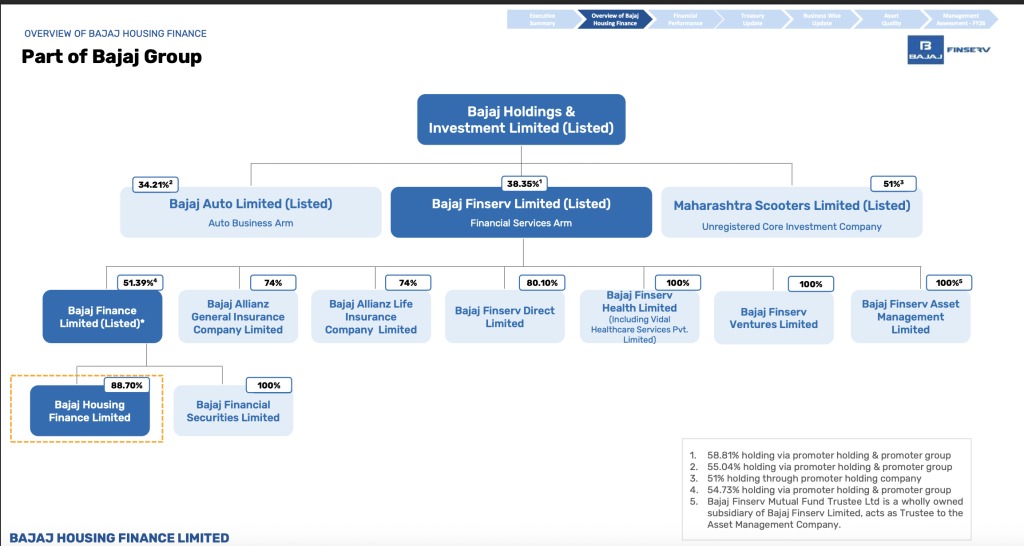

Bajaj Housing Finance Ltd (BHFL)

A fully owned subsidiary of Bajaj Finance, BHFL has rapidly grown to become a serious challenger to banks & NBFCs in the home loan & mortgage finance market.

From salaried home loans to builder financing, from LAP to co-lending — BHFL is shaping itself to ride India’s massive formal housing credit boom.

Also Read: Medi Assist Healthcare Services Ltd — Business Model, Management Vision & 2025-2030 Growth Roadmap

🧩 Company Snapshot

| Parameter | Details |

|---|---|

| Company | Bajaj Housing Finance Ltd (BHFL) |

| Parent | Bajaj Finance Ltd |

| Industry | Housing Finance (HFC) |

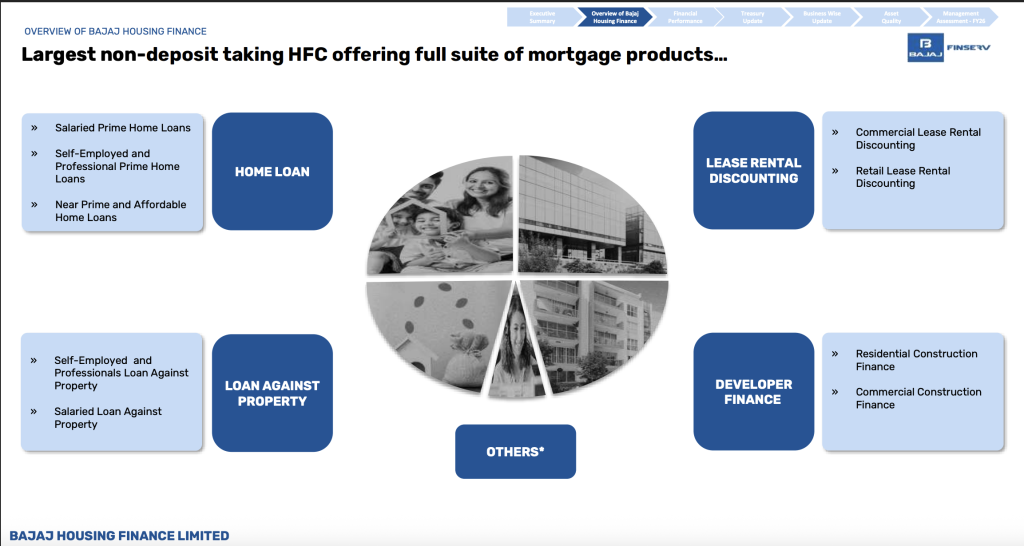

| Business | Home loans, Loan Against Property (LAP), developer loans |

| Backed by | Bajaj Finserv group |

| Credit Rating | AAA (stable) by all major agencies |

| Customer Base | Individuals + self-employed + developer finance |

| Distribution Model | Hybrid — digital + branch + partner network |

Why this matters:

AAA + Bajaj group + digital underwriting = one of the most trusted new-age mortgage lenders in India.

💡 Business Model — How BHFL Makes Money

BHFL follows a secure, asset-backed lending model with deep credit underwriting. Key revenue engines:

1️⃣ Home Loans (Retail Housing Finance)

- Salaried & Professional customers

- Prime credit quality

- Lowest risk mortgage pool in lending ecosystem

- Sticky, long-tenor, predictable cashflow

2️⃣ Loan Against Property (LAP)

- Secured loan against residential/commercial properties

- Targeting entrepreneurs & self-employed

- Higher yields than home loans

3️⃣ Developer/Real Estate Financing

- Structured finance to branded developers

- Last-mile project funding

- High underwriting discipline

BHFL model essence:

Lower risk, high asset quality, strong recovery visibility.

🎯 What Makes BHFL Different

✅ Parentage & Governance

Bajaj Group = conservative underwriting, zero-nonsense compliance.

No aggressive lending culture like some NBFCs pre-COVID.

✅ Tech-Driven Credit Evaluation

Uses digital income assessment, banking analytics & property valuation tech — faster disbursals, yet controlled risk.

✅ Co-lending & Cross-Sell

- Works with Bajaj Finance & banking partners

- Access to premium credit profiles

✅ Funding Advantage

AAA rating = access to low-cost long-term capital

Critical in mortgage industry.

✅ Balanced Mix: Salaried + Self-Employed

Don’t rely only on salaried segment. Diversified base = risk hedging.

🎙 Management Tone

BHFL leadership message has consistently focused on:

“Disciplined growth, asset quality, and long-term profitability.”

“We do not chase volume at the cost of risk.”

“Our priority is to build a high-quality secured book and scale sustainably.”

“Digital underwriting and data stack will drive operating leverage.”

Tone = steady, conservative, scalable.

Exactly what you want in a housing finance lender.

📈 Financial & Market Positioning

- Housing credit market growing ~12–14% CAGR

- India’s mortgage-to-GDP still ~11% vs 40%+ in mature markets

- Urbanization + rising formal income → multi-year credit boom

Bajaj Housing has gone from niche lender → serious challenger to:

- HDFC (now HDFC Bank)

- LIC Housing

- PNB Housing

- Can Fin Homes

- Aavas Financiers

Competitive edge:

Underwriting + AAA funding + Bajaj brand + digital infrastructure.

🧠 Strategic Pillars (2025–2030)

1️⃣ Prime Credit Home Loans

Focus on salaried & stable profiles — lowest credit cost segment.

2️⃣ Growing Self-Employed Book (Controlled)

Large opportunity; but monitored & secured.

3️⃣ Strong Developer Finance

But only with branded developers, project visibility, escrow cashflows.

4️⃣ Tech-Led Origination + AI Underwriting

Bajaj already proven this in consumer finance — now replicated in mortgages.

5️⃣ Liability Management

AAA = long-term bonds, refinance lines, diversified funding pool.

Outcome:

Stable NIM, predictable GNPA/NNPA, scalable risk-adjusted returns.

🔮 Future Growth Drivers

| Driver | Impact |

|---|---|

| Formal housing demand | Rising middle class, urbanisation |

| Affordable housing push | Govt policy tailwind |

| Low mortgage penetration | Structural 10-year runway |

| Digital onboarding | Faster scale, lower operating cost |

| Cross-sell ecosystem | Bajaj Finance + Bajaj Finserv synergies |

Onetrader View:

BHFL has potential to become top-5 housing finance franchise over next 5–7 years.

⚠️ Risks to Track

Credit is simple: mistakes compound faster than interest.

Potential risks:

| Risk | Mitigation |

|---|---|

| Macro slowdown in real estate | Prime segments → low stress |

| Competition in mortgage rates | Tech + brand = pricing power |

| Property price correction | Secured loans + strong LTV buffers |

| Execution risk in developer finance | Only branded projects + escrow |

| Regulatory changes | Bajaj governance + capital cushion |

🎯 Onetrader Verdict

Bajaj Housing Finance =

High-quality secured lender + AAA balance sheet + tech DNA + predictable compounding

This is a Core Portfolio Compounder for long-term investors.

📌 Style: Low-risk compounding

📌 Horizon: 5+ years

📌 Allocation logic: SIP on corrections

📌 Key monitor metrics: GNPA, NNPA, spreads, LTV, growth rate, liability cost

Not flashy multibagger.

Slow, reliable wealth compounder.